Problem 8.03 – Madeoff’s Mortgage

Multinational Business Finance

Eiteman, Stonehill, and Moffett

15th Edition

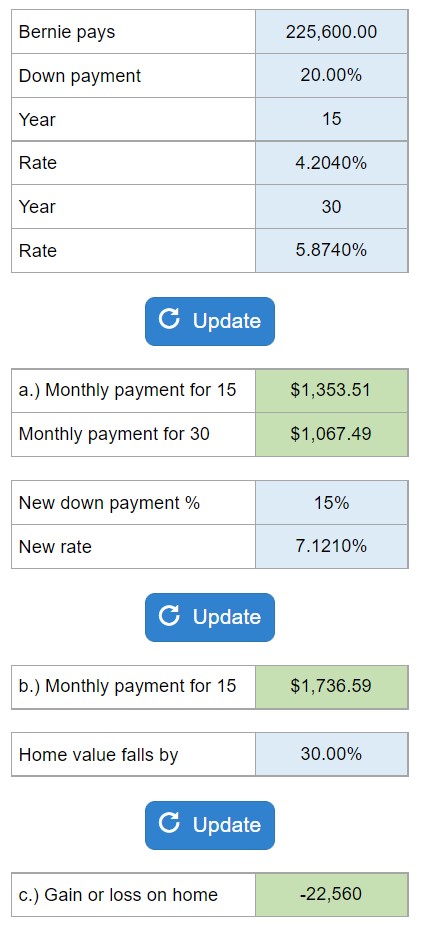

Determine the monthly payment on the house given a 15-year and 30-year mortgage.

Calculator Preview

Your numbers will vary.

Determine the monthly payment on the house given a 15-year and 30-year mortgage.

Your numbers will vary.

Botany Bay has three alternatives to analyze: a fixed rate for 2 years, LIBOR + % which resents every six months, and borrowing fixed for one year, but then having to negotiate for a new one-year loan thereafter.

Your numbers will vary.

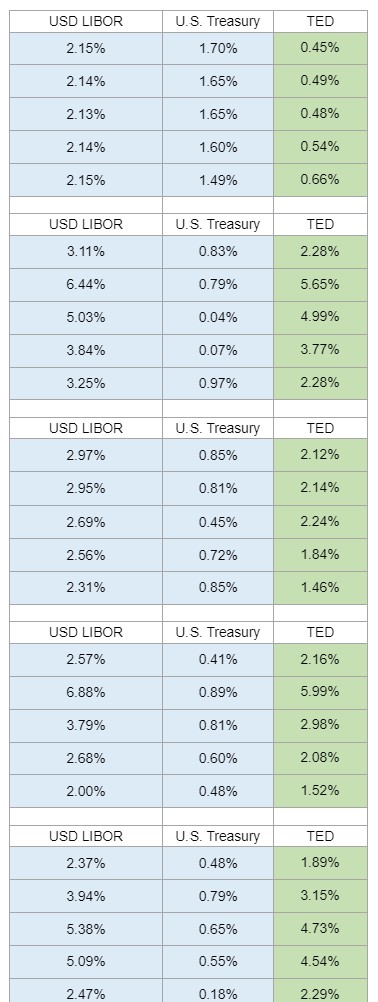

During financial crises, short-term interest rates can change quickly, as seen in the table provided for selected dates in September-October 2008. One measure of the TED spread (Treasury-Eurodollar spread) is the differential between the overnight LIBOR interest rate and the 3-month U.S. Treasury bill rate. The question asks to calculate the TED spread between the two market rates in September and October 2008, determine the narrowest and widest date for the spread, and identify which rate moves the most and why when the spread widens dramatically, demonstrating financial anxiety or crisis.

Your numbers will vary.

Determine the gain or loss on the interest rate futures.

Your numbers will vary.

Given that the firm must pay float-rate interest and it wishes to lock in interest rate payments using interest rate futures, determine the gain or loss on the position at various possible floating interest rates.

Your numbers will vary.

Determine the savings or costs for the swap given that LIBOR rises or falls by various basis points.

Your numbers will vary.

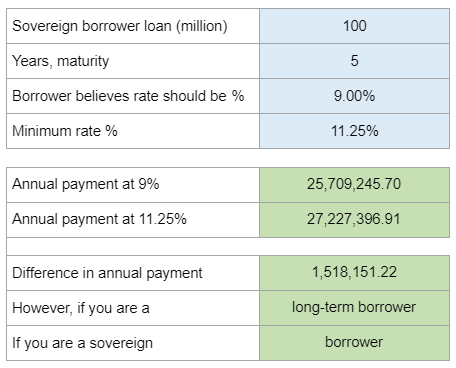

Calculate the annual payment for a loan with a fixed maturity for a sovereign borrower, taking into account an amortizing structure. Consider the impact of negotiating for various interest rates given by international banks.

Your numbers will vary.

Determine the loan payment on the six-year loan, and amortize the loan. Then, suppose the firm can extend the loan another two years by restructuring, determine the new loan payment and complete the amortization schedule.

Your numbers will vary.

Calculate the cost of unwinding the swap some number of year(s) has passed, given the updated fixed interest rates and spot exchange rate for MedStat’s cross-currency swap.

Your numbers will vary.

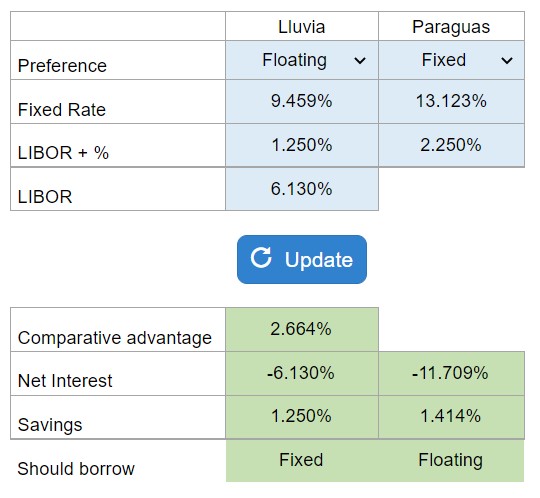

Determine the comparative advantage, the net interest after the swap, and the savings to both firms.

Your numbers will vary.