Problem 8.06 – Heather O’Reilly

Multinational Business Finance

Eiteman, Stonehill, and Moffett

15th Edition

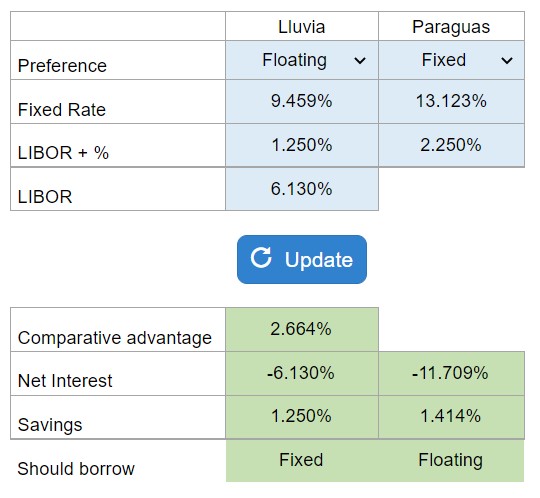

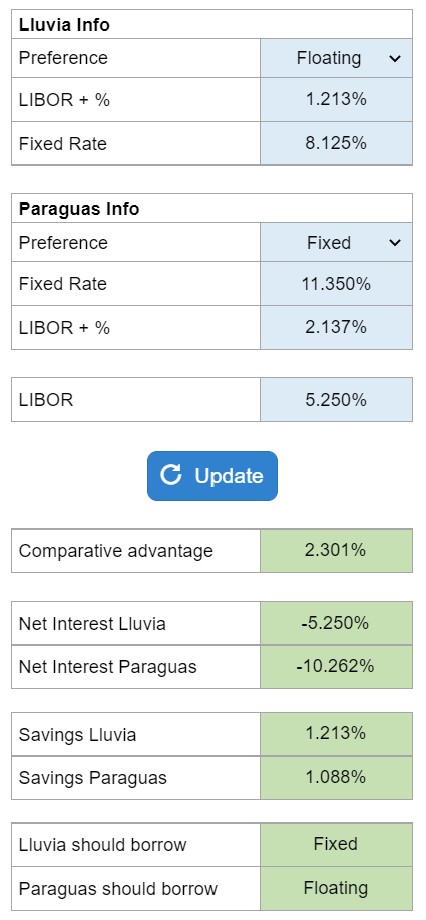

Determine the savings or costs for the swap given that LIBOR rises or falls by various basis points.

Calculator Preview

Your numbers will vary.