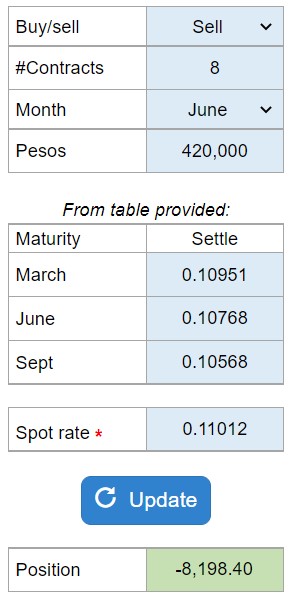

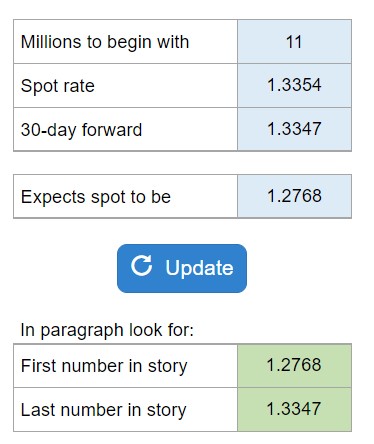

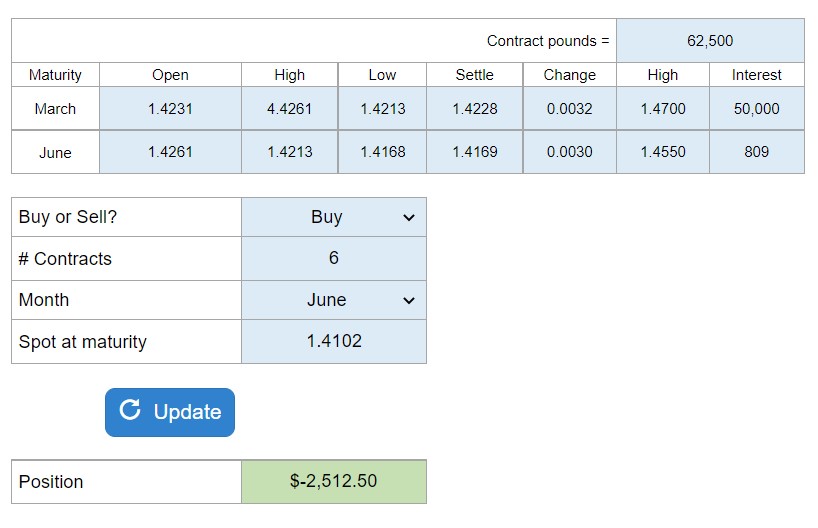

Problem 7.01 – Tony Begay at Saguaro Funds

Multinational Business Finance

Eiteman, Stonehill, and Moffett

15th Edition

Determine the value of Tony’s position if Tony buys or sells a certain number of contracts on the British pound.

Calculator Preview

Your numbers will vary.