E 9.14 – Campbell Corporation

Intermediate Accounting

Spiceland, Nelson, and Thomas

10th Edition

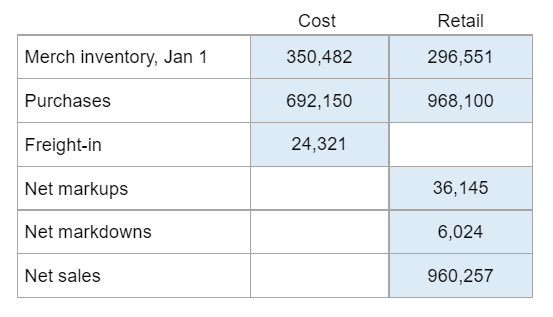

Determine the inventory by applying the conventional retail method.

Calculator Preview

Your numbers will vary.

Determine the inventory by applying the conventional retail method.

Your numbers will vary.

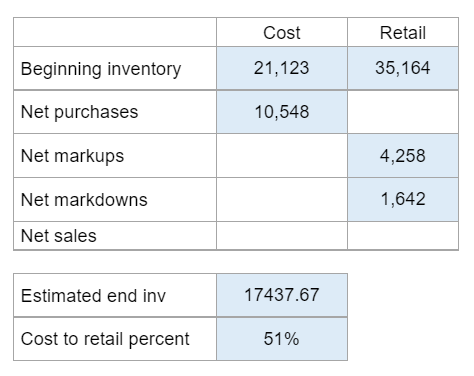

Given the beginning inventory, net purchases, markups, and markdowns along with estimated ending inventory and cost to retail percentage… find the net purchases at retail and net sales.

Your numbers will vary.

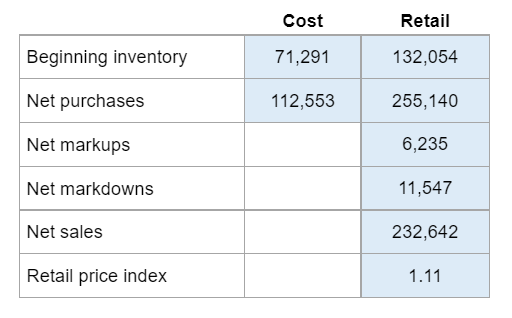

Given the beginning inventory, net purchases, markups, markdowns, sales, and the retail price index… calculate the ending inventory and cost of goods sold.

Your numbers will vary.

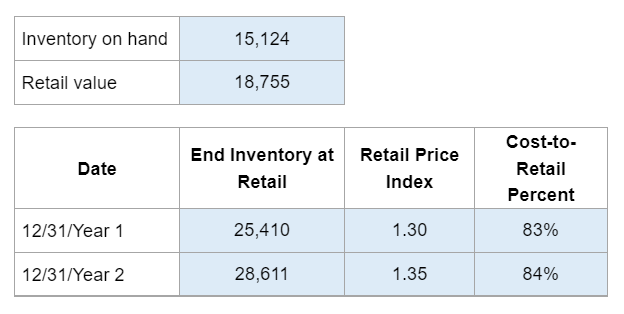

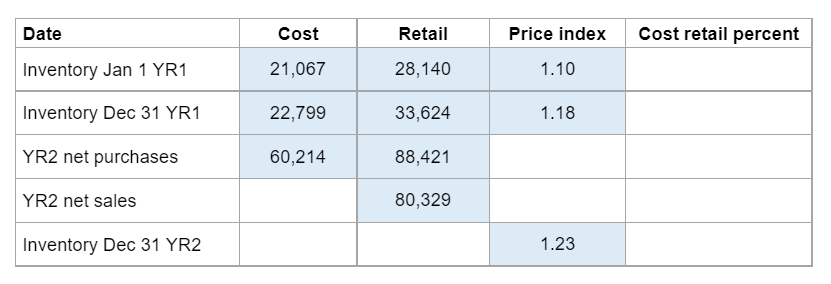

Given the inventory at hand and retail value along with the ending inventory at retail, retail price index, and cost to the retail percentage for two years… calculate both the cost to the retail percentage at the beginning of the first year and inventory value at the end of both years.

Your numbers will vary.

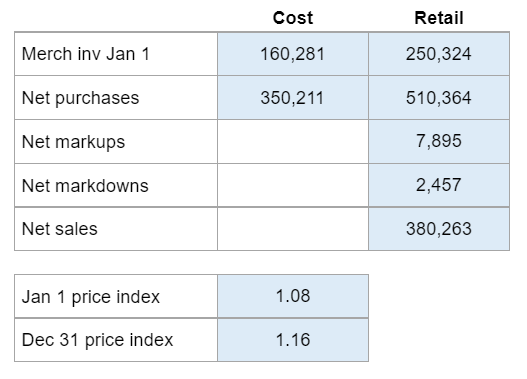

Given the merchandise inventory at the beginning of the year, purchases, markups, markdowns, net sales, and price index at the beginning and end of the year… calculate the ending inventory and cost of goods sold.

Your numbers will vary.

Given a chart regarding inventory with missing values… determine the missing data.

Your numbers will vary.

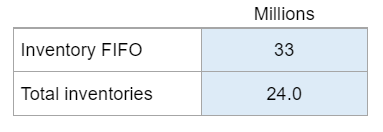

Given the inventory at year-end using both FIFO method and average cost method… prepare a journal entry for the adjustment.

Your numbers will vary.

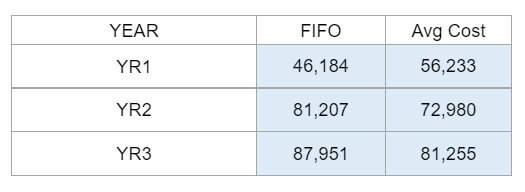

Prepare the journal entry to adjust to avg cost method. How much is cost of goods sold adjustment on the revised income statement?

Your numbers will vary.

Given the amount that was overstated and understated in consecutive days … determine the effect on retained earnings along with preparing a journal entry.

Your numbers will vary.

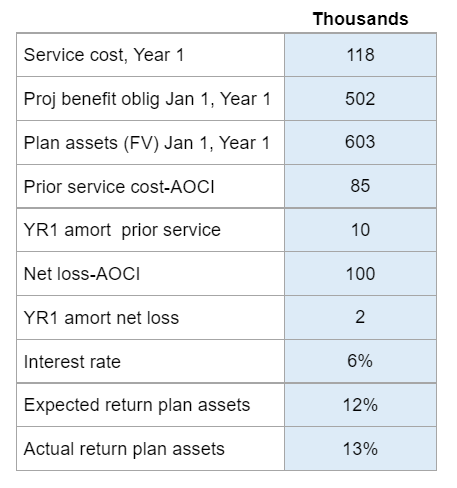

Given data regarding their pension plan… determine the pension expense for the year.

Your numbers will vary.