Problem 18-05, Relative Tax Advantage of Corporate Debt

Principles of Corporate Finance

Brealey, Myers, and Allen

13th Edition

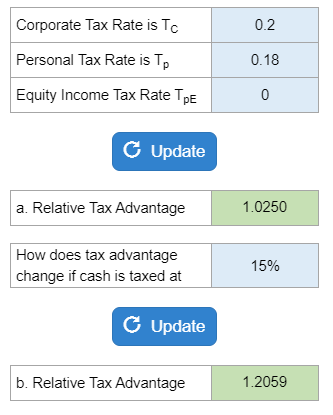

Calculate the relative tax advantage of debt.

Calculator Preview

Your numbers will vary.

Calculate the relative tax advantage of debt.

Your numbers will vary.

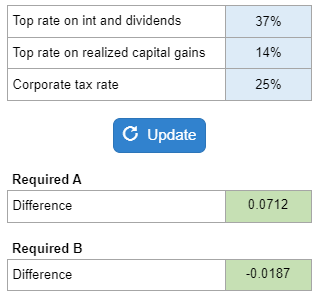

Given the personal tax rate on dividends and capital gains along with the corporate tax rate… find the difference between total taxes paid on debt and total taxes paid on equity.

Your numbers will vary.

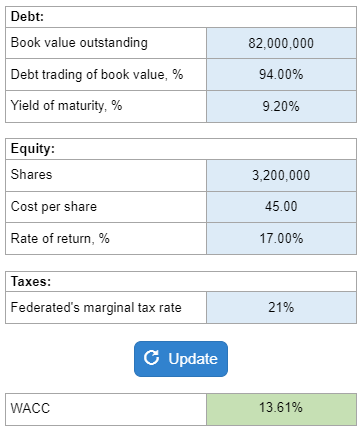

Given the book value of debt outstanding and the percent it is trading at, the shares of equity and the cost per share with the rate of return, and the marginal tax rate… calculate the WACC for Federated Junkyard.

Your numbers will vary.

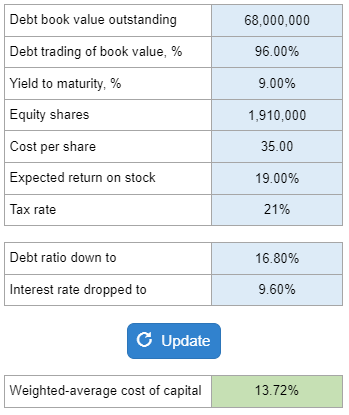

You are given the book value of debt and percent it is trading at, the yield to maturity, the shares of equity, the cost per share, the expected return, tax rate, and debt ratio. If the firm moves to a more conservative debt policy, calculate the new WACC using the three-step method.

Your numbers will vary.

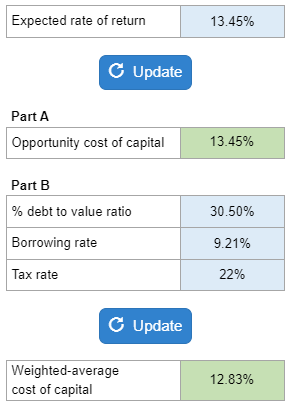

Given the expected rate of return for an all-equity financed firm and ask you to determine the opportunity cost of capital. Then they give you the debt to-value ratio, the borrowing rate, and the tax rate… determine the weighted average cost of capital.

Your numbers will vary.

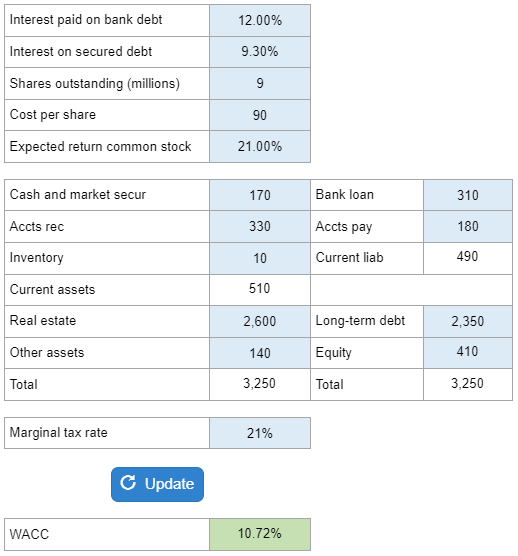

Given the interest rate on bank debt, the rate on secured debt, the shares outstanding, the price per share, the expected return, and a balance sheet along with a tax rate… calculate the WACC.

Your numbers will vary.

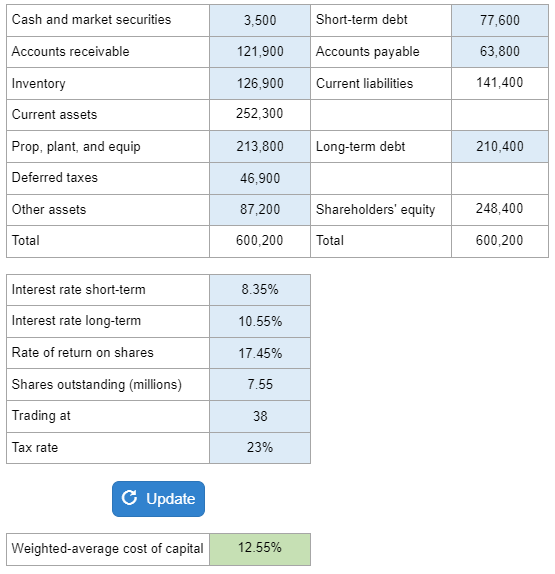

Given a balance sheet along with short-term and long-term interest rates, the return on shares, the number of shares outstanding and the amount it is trading at, and the tax rate… calculate the WACC.

Your numbers will vary.

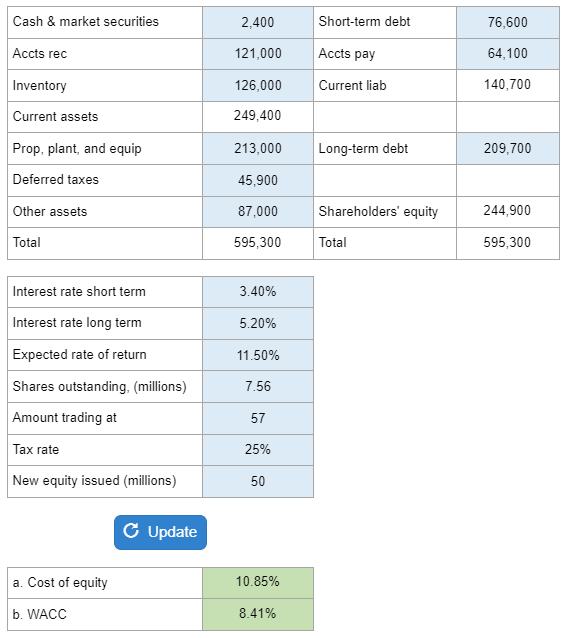

Given a balance sheet along with interest rates for debt, expected rate of return, shares outstanding, amount it is trading at, tax rate, and the new equity issued… determine the cost of equity and WACC after the capital restructuring where the company issues new equity to retire debt.

Your numbers will vary.

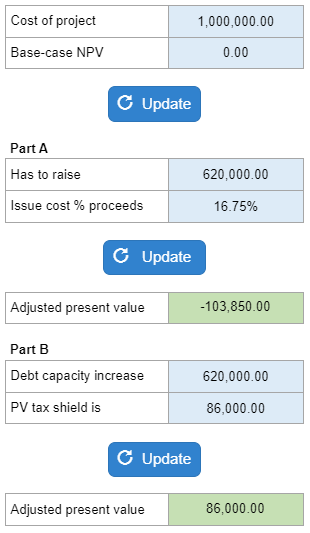

Given the base-case NPV of a project and give you two different firm investments… find the adjusted present value, APV.

Your numbers will vary.

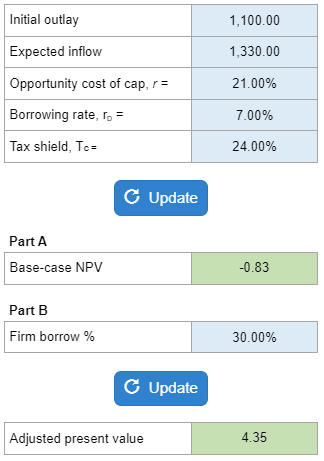

Given the initial outlay of a project, the expected cash inflow, the opportunity cost of capital, the borrowing rate, and the tax shield per dollar… determine the project’s base-case NPV along with the APV accounting for the interest tax shields.

Your numbers will vary.