Cycle Project 2, AP5.01, AP6.01 & AP7.01 – Great Adventures

Financial Accounting

Spiceland, Thomas, and Herrman

05th Edition and 06th Edition

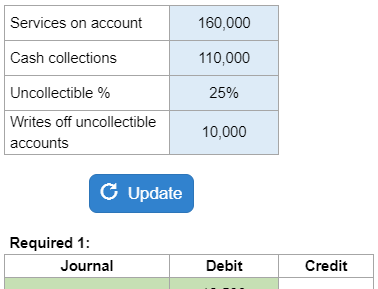

Prepare journal entries, partial balance sheets, evaluate the allowance of uncollectables, create a partial income statement with sales revenues, cost of goods sold, and gross profit. Calculate cost of goods sold and ending inventory using FIFO.

Then, using information about the net realizable value, reestimate the partial income statement and balance sheets. Finally, create a depreciation schedule showing depreciation and book values and record adjusting entries for depreciation and insurance.