Quiz Ch 09 – T/F Significance of Times-Interest-Earned Ratio

Financial Accounting

Thomas, Tietz, and Harrison

12th Edition

The times-interest-earned ratio reflects the company’s capacity to cover interest costs.

The times-interest-earned ratio reflects the company’s capacity to cover interest costs.

The effective-interest method generates varying interest expenses for each interest payment made during the bond’s life.

GAAP permits the straight-line amortization method for bond discounts and premiums only when the resulting amounts are relatively similar to those obtained through the effective-interest method.

The straight-line amortization method is considered the most theoretically accurate approach to amortizing bond discounts and premiums as it acknowledges the influence of the time value of money on interest expenses recognized in each interest payment period.

Which method of amortizing a bond discount or premium is considered the most theoretically correct?

What is the accounting treatment of the Premium on Bonds Payable account on the balance sheet?

Where would the retirement of callable bonds below face value appear on a cash flow statement?

What is the definition of secured bonds?

Under what condition would the lease for equipment signed by Wayne Technical Corporation be classified as a finance lease?

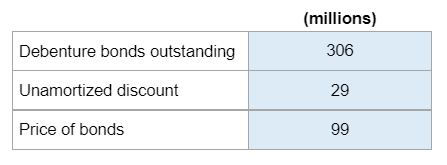

Given the debenture bonds outstanding, unamortized discount, and price of bonds – find the gain/loss on retirement of bonds and how it would be shown in the financial statements.

Your numbers will vary.