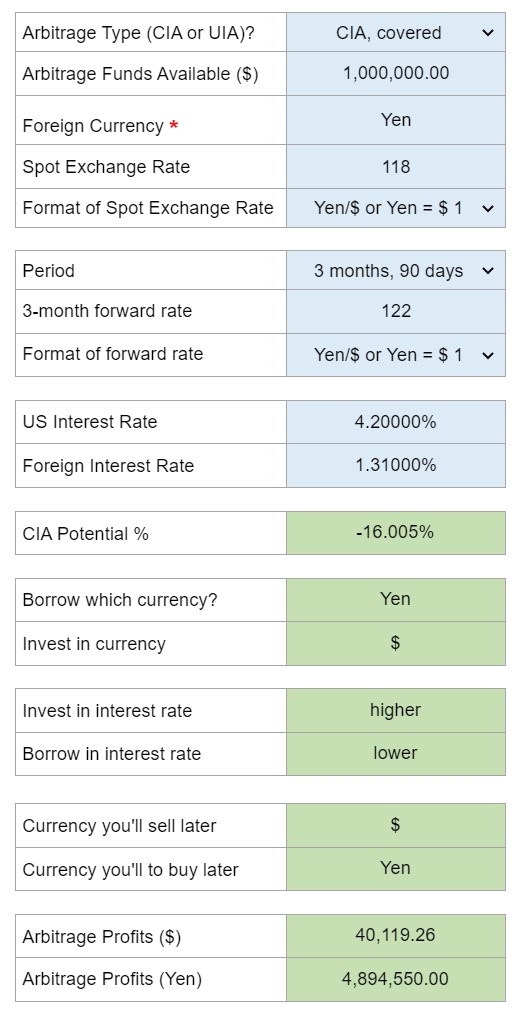

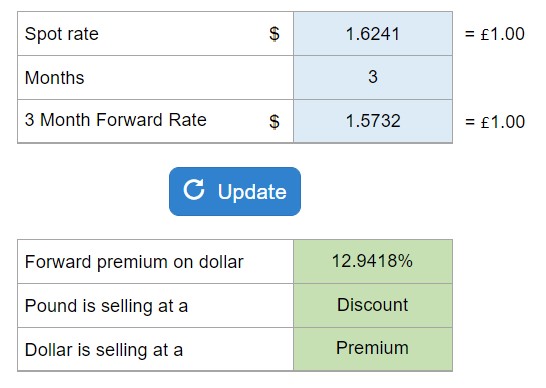

Problem 5.16 – Direct Forward Discount on the Dollar

Multinational Business Finance

Eiteman, Stonehill, and Moffett

15th Edition

Determine the forward premium or discount on the dollar and the pound using a 360-day year.

Calculator Preview

Your numbers will vary.