P 16.04 – Zekany Corporation

Intermediate Accounting

Spiceland, Nelson, and Thomas

10th Edition

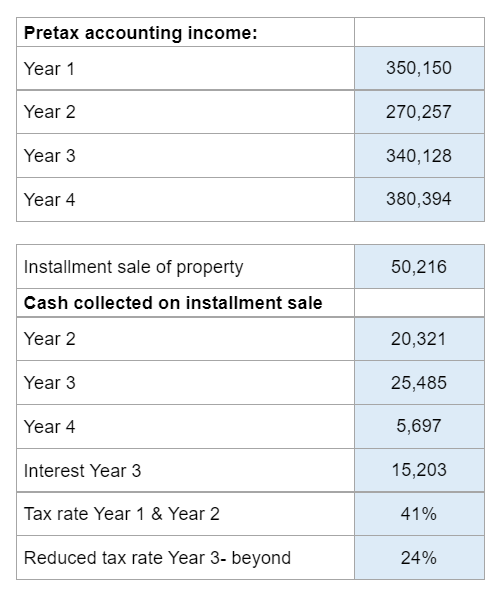

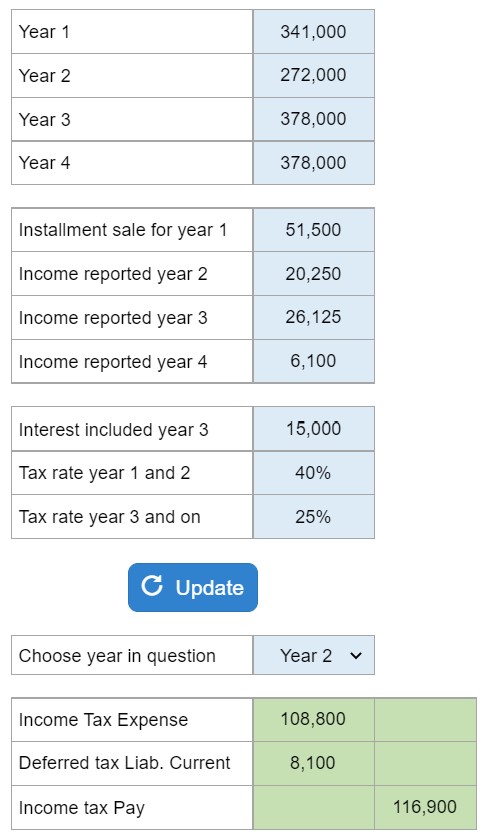

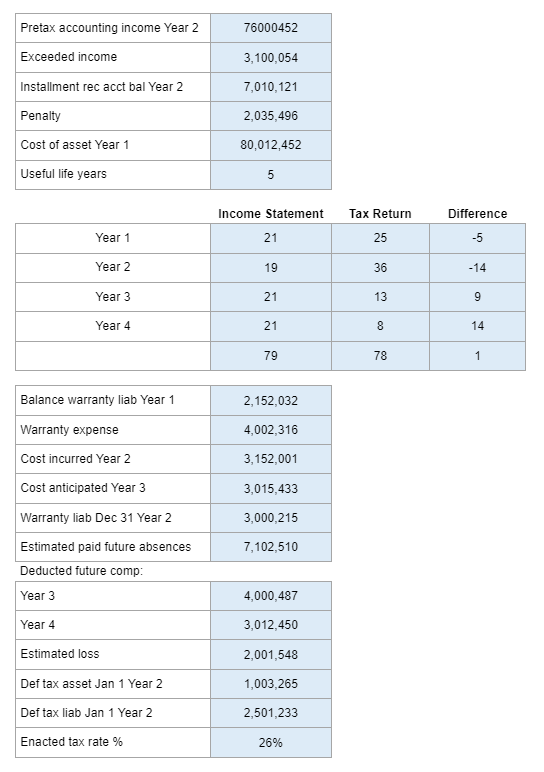

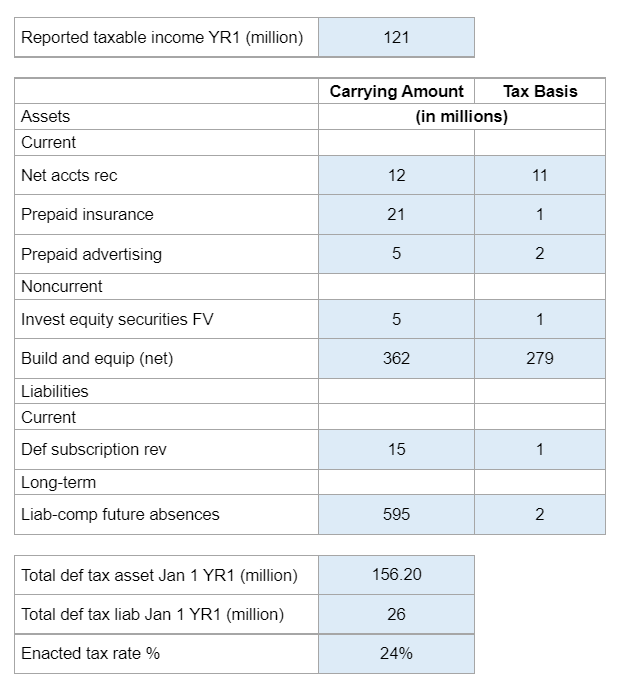

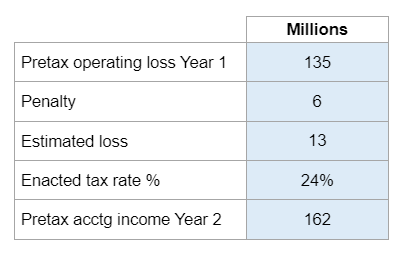

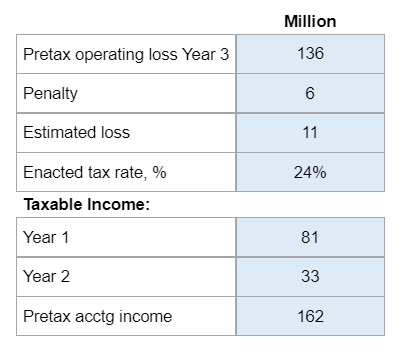

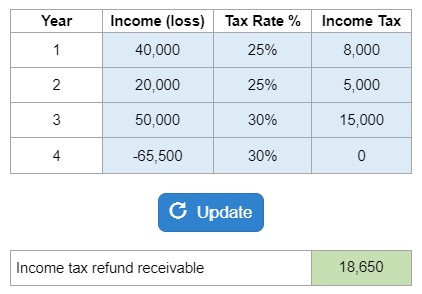

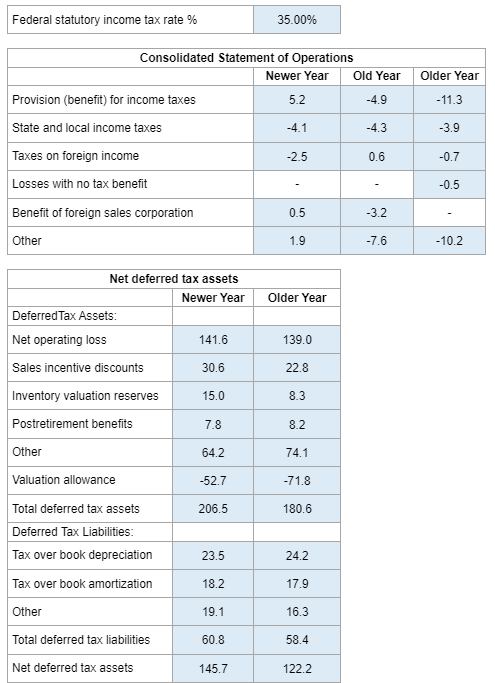

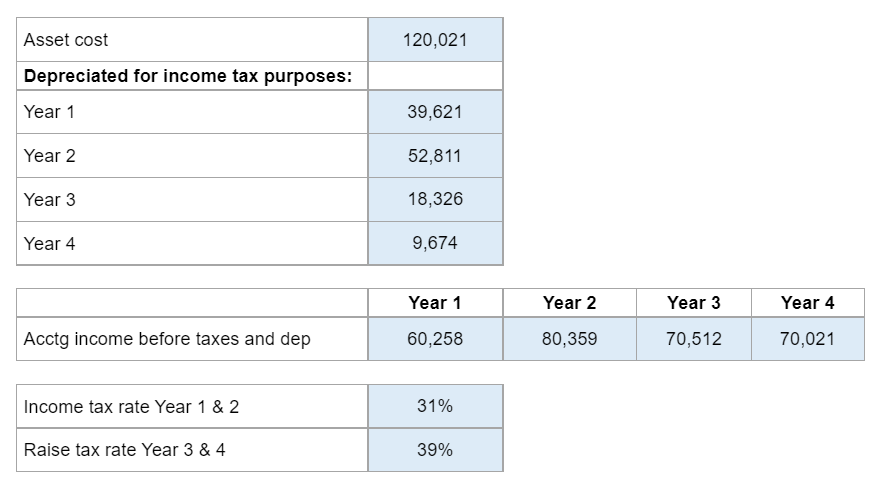

Given the asset cost, the depreciation per year, the accounting income before taxes, and depreciation…. prepare journal entries for the income tax.

Calculator Preview

Your numbers will vary.