Quiz – Lacy’s Linen Mart

Intermediate Accounting

Spiceland, Nelson, and Thomas

10th Edition

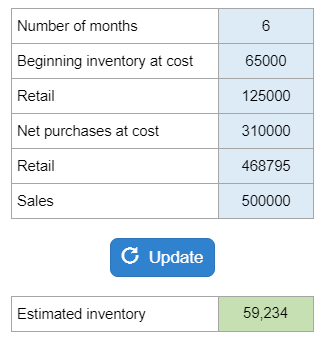

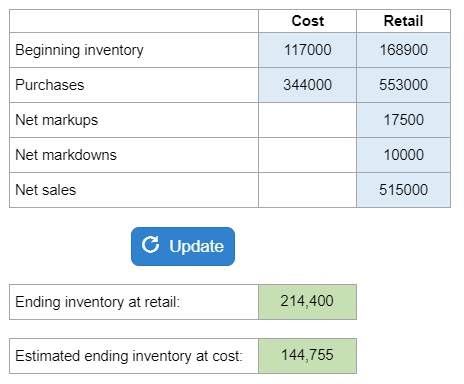

Given beginning inventory and purchases along with sales, they ask you to determine the estimated inventory.

Calculator Preview

Your numbers will vary.

Given beginning inventory and purchases along with sales, they ask you to determine the estimated inventory.

Your numbers will vary.

In applying LCM, market value can’t be:

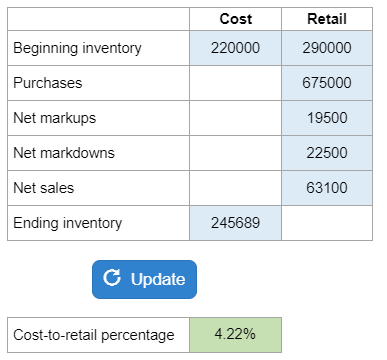

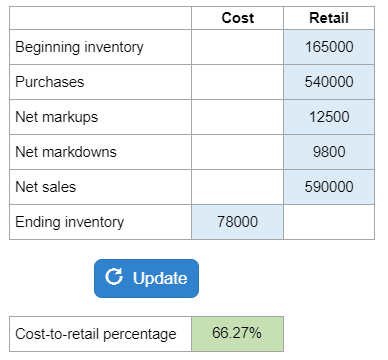

Determine the cost-to-retail percentage used by the company, given the beginning inventory, purchases, markups, markdowns, sales, and inventory.

Your numbers will vary.

Given the year-end inventory on a LIFO basis and other information regarding inventory, they ask you to determine the reported value of the inventory.

Your numbers will vary.

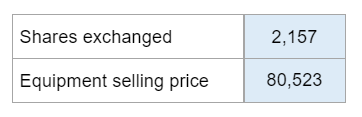

What does the journal entry to record the equipment transaction include?

Your numbers will vary.

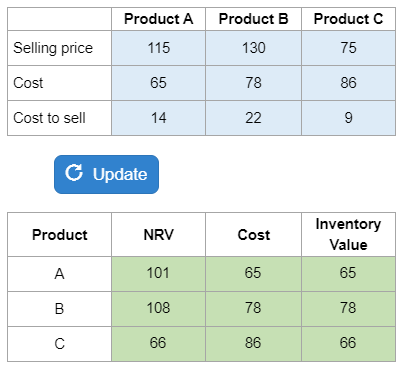

Given the selling price, costs, and costs to sell, they ask you to determine the inventory value of three different products.

Your numbers will vary.

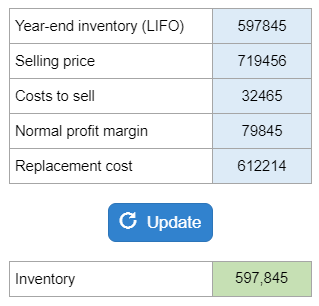

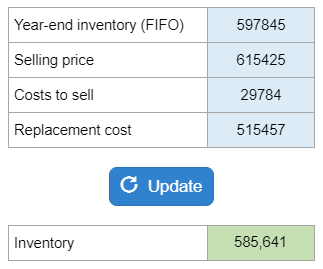

Given the year-end inventory, the selling price, costs to sell, and replacement cost, they ask you to determine what inventory should be reported.

Your numbers will vary.

They ask you to estimate the LIFO cost ending inventory given beginning inventory, purchases, markdowns, markups, and sales.

Your numbers will vary.

Calculate the cost-to-retail percentage when given the beginning inventory, purchases, markups, markdowns, sales, and ending inventory.

Your numbers will vary.

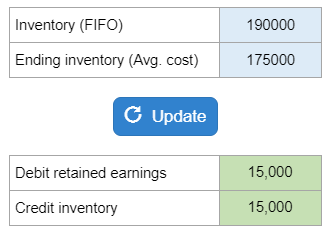

Given the amount that inventory was reported as and the amount that they are changing it to under the new method, they ask you to determine what journal entry would be recorded.

Your numbers will vary.