BE 9.01 – Ross Electronics

Intermediate Accounting

Spiceland, Nelson, and Thomas

10th Edition

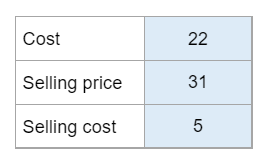

Given the cost, selling price, and selling cost… find unit value.

Calculator Preview

Your numbers will vary.

Given the cost, selling price, and selling cost… find unit value.

Your numbers will vary.

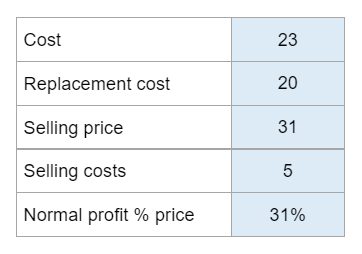

Given the cost, replacement cost, selling price, and normal profit price… find the unit value.

Your numbers will vary.

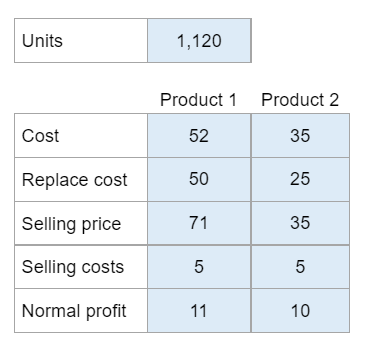

Given units, cost, replacement cost, sell price, sell cost, and normal profit… find the effect of LCM adjustment and cost of the market.

Your numbers will vary.

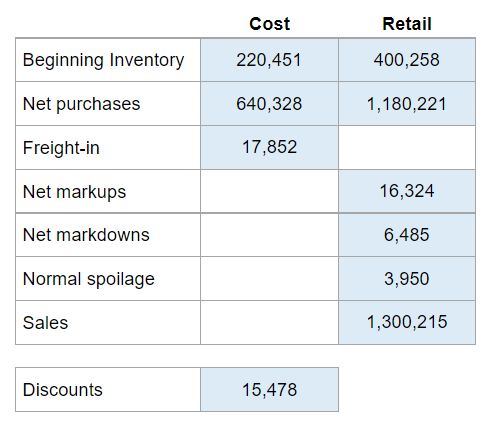

Given the beginning inventory, net purchases, freight-in, markups, markdowns, spoilage, sales, and discounts… calculate the ending inventory and cost of goods sold using the conventional method.

Your numbers will vary.

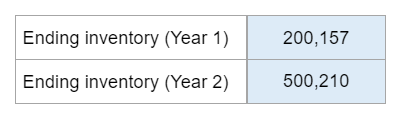

Given ending inventory for both years… find the retained earnings for the beginning of next year.

Your numbers will vary.

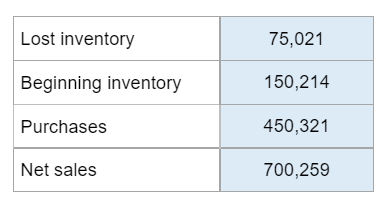

Given the lost inventory, beginning inventory, purchases, and net sales… calculate the gross profit ratio.

Your numbers will vary.

For each of these 2021 inventory errors occurring, state the effect of the error on cost of goods sold, net income, and retained earnings using the following notation: understated (U), overstated (O), or no effect (NE). Also, use the following assumptions: the error is not discovered until 2022 and that a periodic inventory system is used. Income taxes can be ignored.

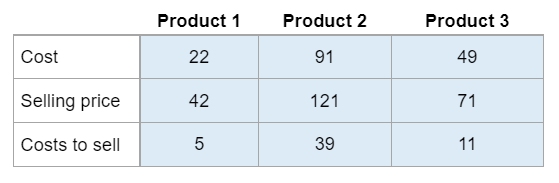

Given the selling price, cost, and the cost to sell for three different products… find the product cost for each and the per-unit value.

Your numbers will vary.

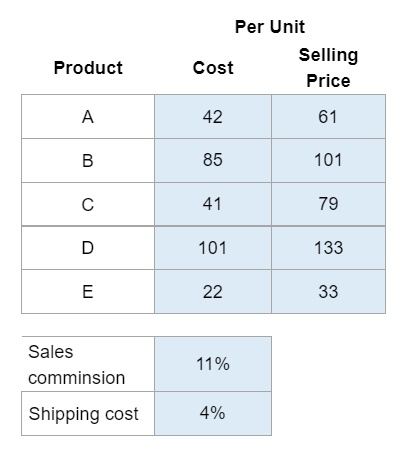

Given the cost per unit and selling price per product… make the net realizing table.

Your numbers will vary.

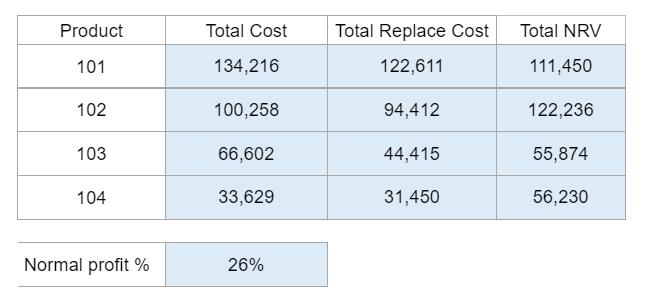

Given you the products, their total cost, total replacement cost, and total net realizable value… determine the carrying value and the adjusting journal entry. For part 1, use the lower of cost or market (LCM) rule.

Your numbers will vary.