Concept 21.4-2 Black-Scholes doesn’t require…

Fundamentals of Corporate Finance

Berk, DeMarzo, and Harford

05th Edition

The Black-Scholes formula doesn’t require us to know the _____.

The Black-Scholes formula doesn’t require us to know the _____.

What is a protective put written on a portfolio known as?

A share of stock is a ______ option written on the assets of the firm with the strike equal to ___.

Debt holders of a corporation can be thought of as owning the firm but having ___ a call option on the assets of the firm with the strike equal to ___.

Equity holders have the incentive to ___ the volatility of the firm, which is a cost to ___.

Identify the false statement regarding options.

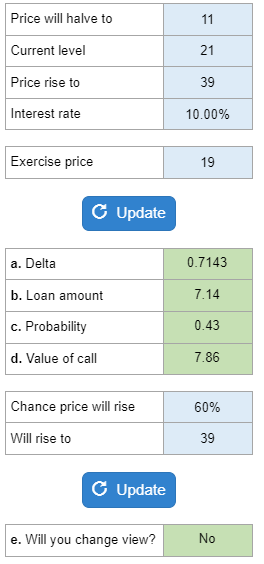

Determine the delta of a one-year call option, the risk-neutral probability that Ragwort stock will rise, and if you would change your view about the value of the option.

Your numbers will vary.

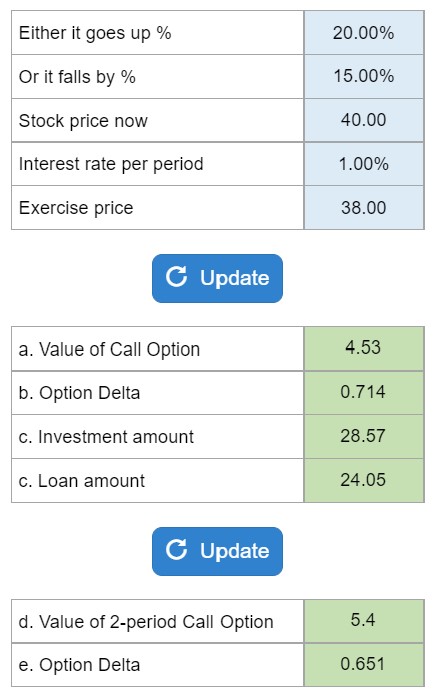

Given the potential increase or decrease in the stock price, the current stock price and the interest rate, determine the value of a call option, the option delta, the amount to be invested in the stock and the amount to be borrowed.

Your numbers will vary.

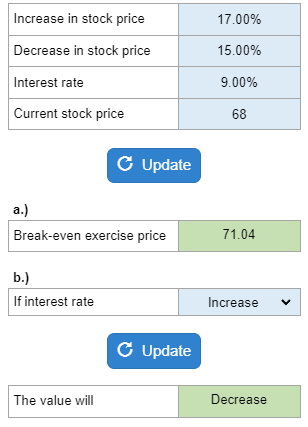

Given the possible increase and decrease in stock price, the interest rate, and the current stock price… determine the break-even price along with whether the value will increase or decrease with a change in interest rate.

Your numbers will vary.

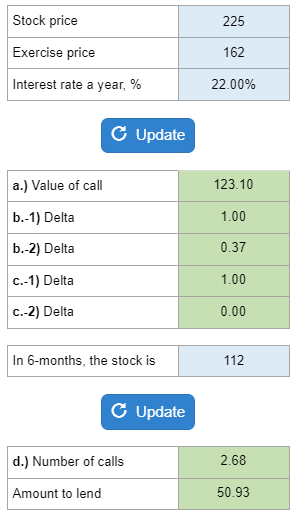

Given the stock price, exercise price, and interest rate… determine the value of the Buffelhead call, the option delta when a call is certain to be and not be exercised, and calculate the option delta for the second six months if the stock price rises and fall.

Your numbers will vary.