Problem 8.04 – TED Spread Global Credit Crisis

Multinational Business Finance

Eiteman, Stonehill, and Moffett

16th Edition

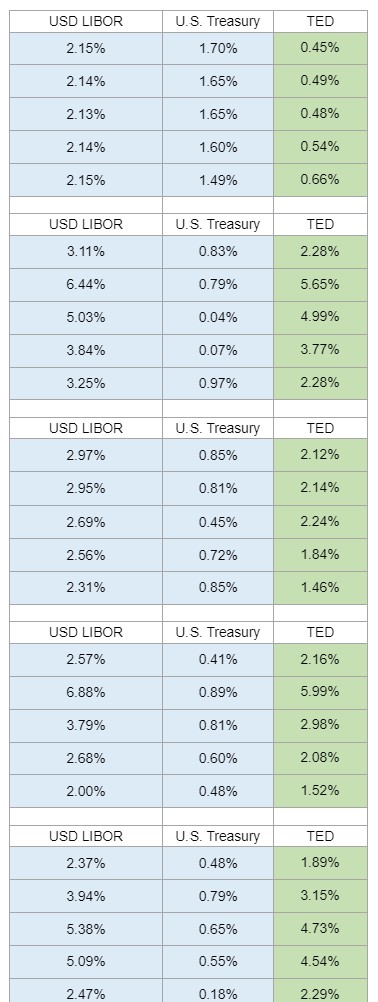

During financial crises, short-term interest rates can change quickly, as seen in the table provided for selected dates in September-October 2008. One measure of the TED spread (Treasury-Eurodollar spread) is the differential between the overnight LIBOR interest rate and the 3-month U.S. Treasury bill rate. The question asks to calculate the TED spread between the two market rates in September and October 2008, determine the narrowest and widest date for the spread, and identify which rate moves the most and why when the spread widens dramatically, demonstrating financial anxiety or crisis.