Problem 3-13, Durations & Volatilities of A, B, and C

Principles of Corporate Finance

Brealey, Myers, and Allen

13th Edition

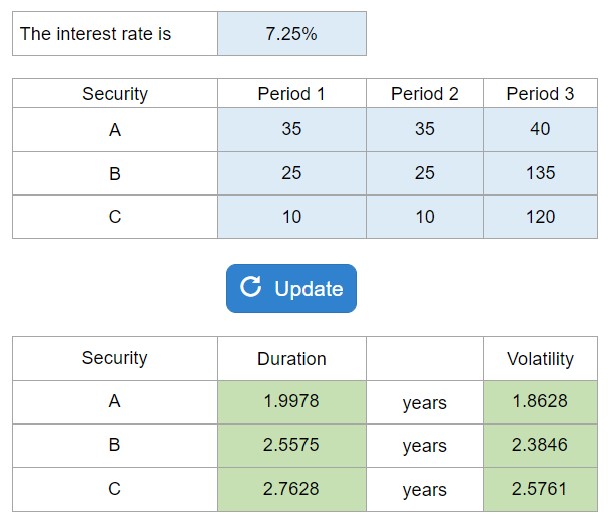

Compute the durations and volatilities of securities A, B, and C.

Calculator Preview

Your numbers will vary.

Compute the durations and volatilities of securities A, B, and C.

Your numbers will vary.

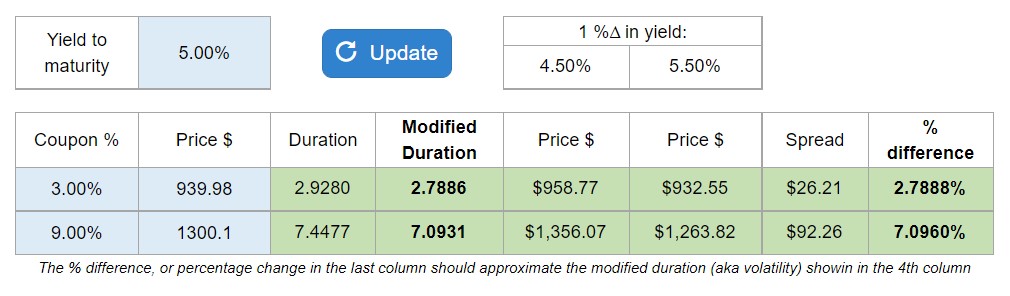

Compute the durations and modified durations for the bonds. Use the modified duration to estimate the percent change in the value of the bond given a 1% change in interest rates.

Your numbers will vary.

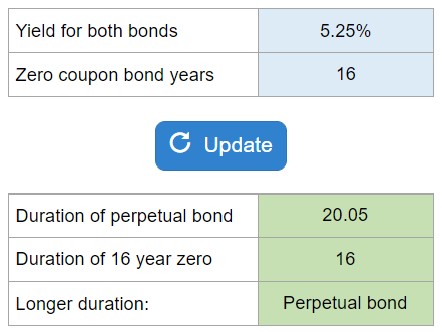

Determine the duration of a perpetual bond and zero-coupon bond. Which has a longer duration?

Your numbers will vary.

In the market for U.S. Treasury bonds, what comes first and what comes after? Spot rates, yields, bond prices? How are they related?

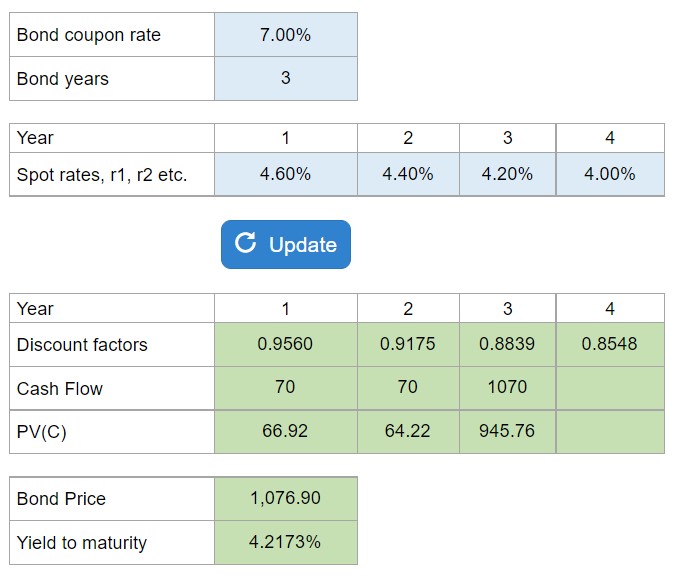

Given a list of spot rates, calculate the discount factors, bond prices, and yields to maturity for various bonds. NOTE: They might ask you for 3 bonds, A, B, and C. Just update the top two inputs, the coupon rate and the total years applicable for each bond, and just press update. Do this for A, then B, and finally for C.

Your numbers will vary.

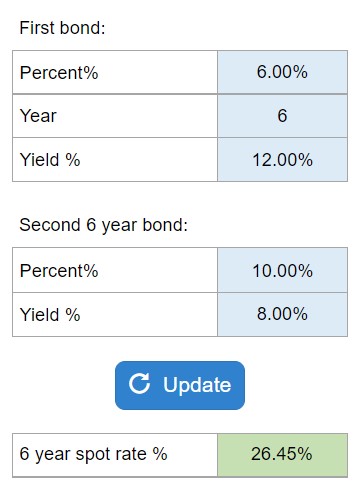

Given coupon rates and yields of two bonds that have the same maturity, compute the spot rate. This solver will also work if they ask you for yield to maturity on a zero-coupon bond, which is the same as the spot rate.

Your numbers will vary.

Determine the shape of the term structure of interest rates given information about yields on high-coupon bonds and low-coupon bonds. Is the term structure upward or downward sloping?

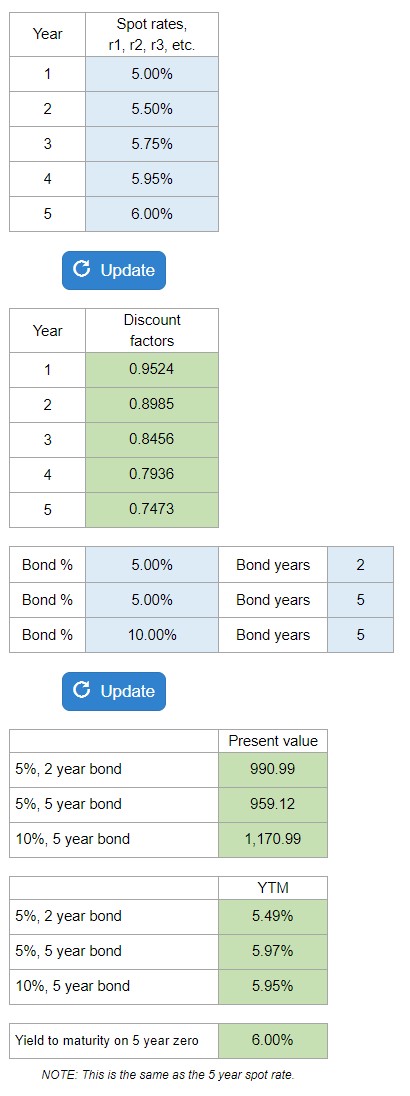

Given estimated spot rates, r1, r2, r3, etc., you are asked to determine the discount factors and bond prices (present values), and yields. You can also infer the spot rate on a 5-year bond (the yield to maturity on a zero-coupon bond)… this solver does it ALL! Check out the preview image to make sure it’ll work for you!

Your numbers will vary.

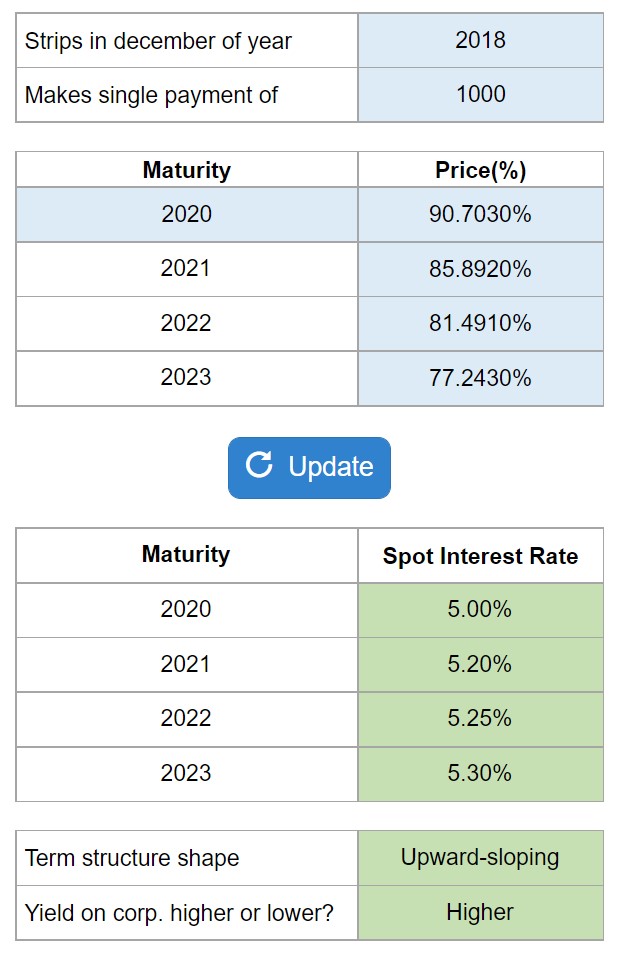

Calculate the spot interest rates for December in each year, then determine the shape of the term structure of interest rates.

Your numbers will vary.

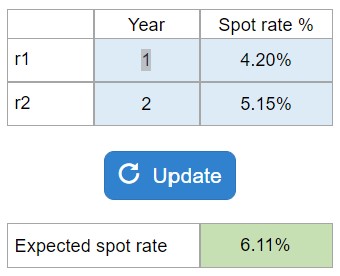

Given spot rates of various maturities, determine the expected interest rate in the future.

Your numbers will vary.