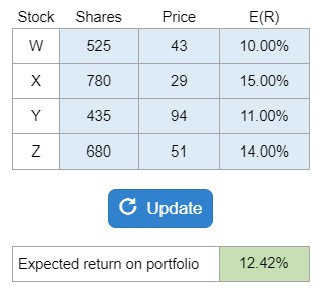

Problem 11.24 – Stock W, X, Y, & Z

Essentials of Corporate Finance

Ross, Westerfield, and Jordan

10th Edition

Given the shares, price, expected return, and weights on stocks W, X, Y, and Z… find the expected return on the portfolio.

Calculator Preview

Your numbers will vary.