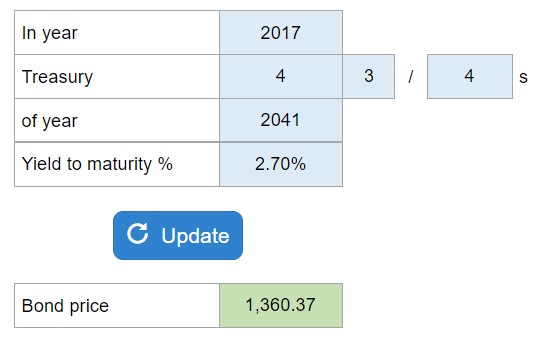

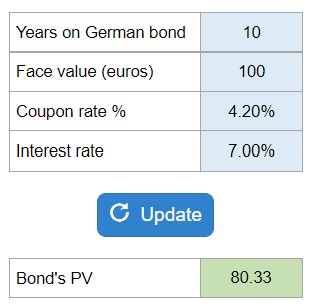

Problem 3-04, German bond

Principles of Corporate Finance

Brealey, Myers, and Allen

13th Edition

Determine the PV of the German bond (in euros). Experts Have Solved This Problem Please login or register to access this content.

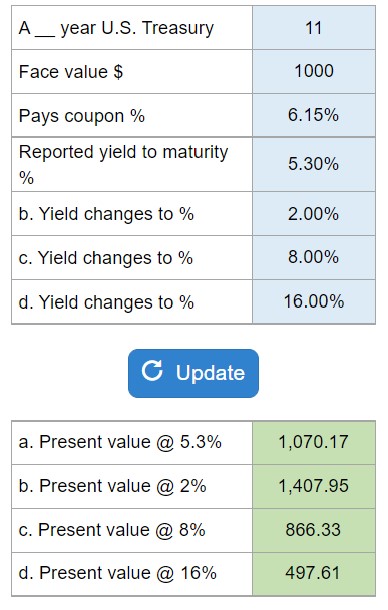

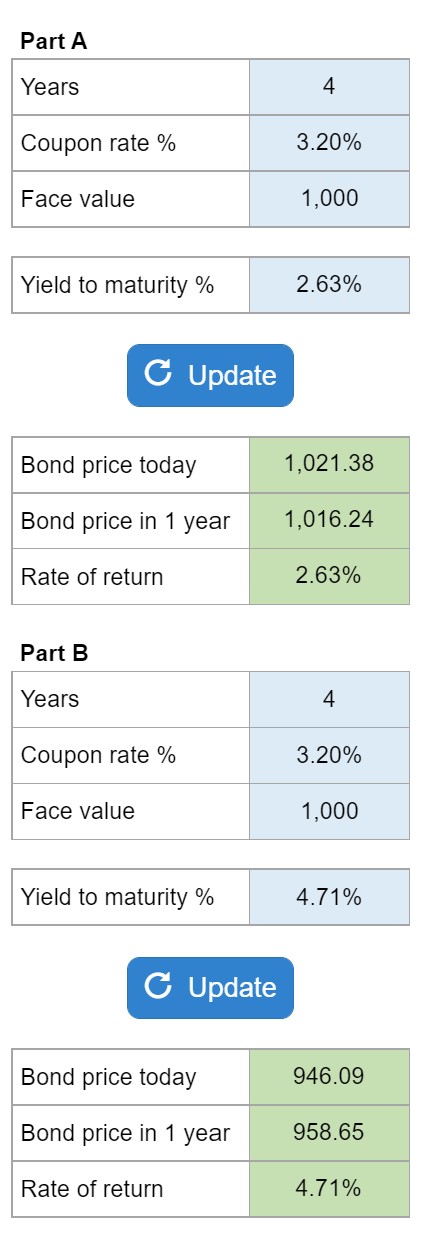

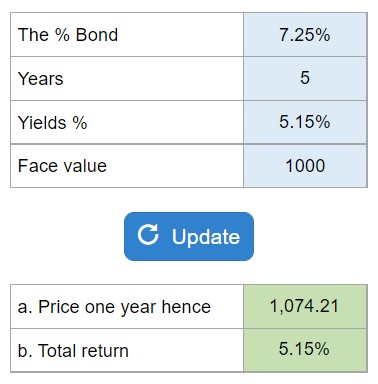

Calculator Preview

Your numbers will vary.