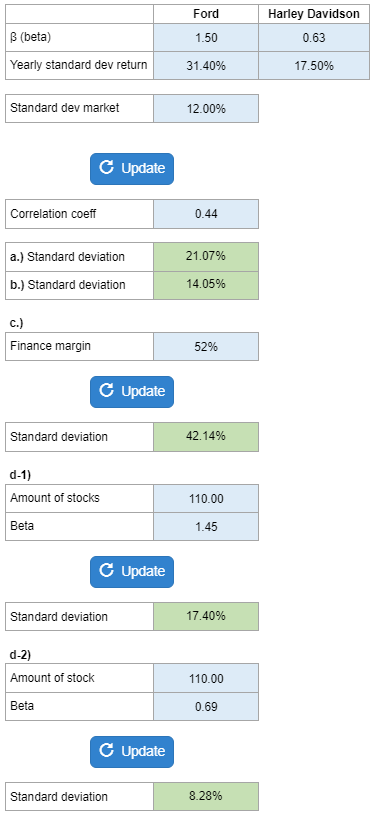

Problem 7-25, Ford & Harley Davidson

Calculator Preview

Your numbers will vary.

Difficulty – Medium

Given the beta and standard deviation of return for two different companies along with the standard deviation of the market... determine the standard deviation of the portfolio given different weights of investment on each stock.

Experts Have Solved This Problem

Please login or register to access this content.