Problem 7.19 – Interest Rate Risk and Bond Price Changes for Different Maturities

Calculator Preview

Your numbers will vary.

Difficulty – Medium

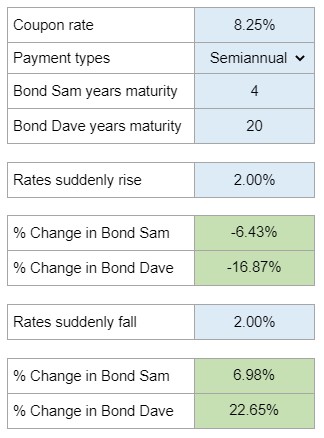

Calculate the percentage change in the price of two bonds with the same coupon rate, payment frequency, and par value but different maturities, given a sudden increase or decrease in interest rates. Illustrate the results by graphing bond prices against YTM and discuss the interest rate risk of longer-term bonds.

Experts Have Solved This Problem

Please login or register to access this content.