Problem 3-24 & 3-25, Spot rates and yields

Calculator Preview

Your numbers will vary.

Difficulty – Medium

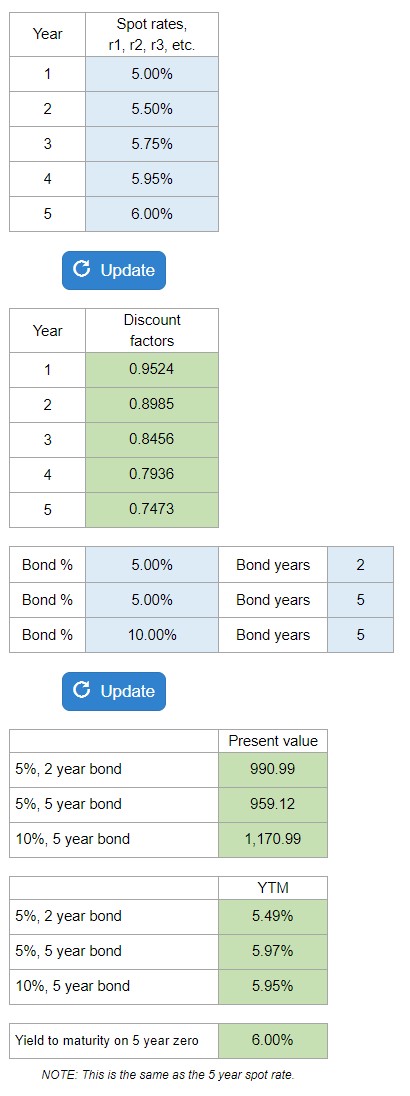

Given estimated spot rates, r1, r2, r3, etc., you are asked to determine the discount factors and bond prices (present values), and yields. You can also infer the spot rate on a 5-year bond (the yield to maturity on a zero-coupon bond)... this solver does it ALL! Check out the preview image to make sure it'll work for you!

Experts Have Solved This Problem

Please login or register to access this content.