Quiz – Understating Inventory

Intermediate Accounting

Spiceland, Nelson, and Thomas

10th Edition

When a company understates its count of it’s ending inventory in the first year and it reports inventory in the second year, which of these is true?

When a company understates its count of it’s ending inventory in the first year and it reports inventory in the second year, which of these is true?

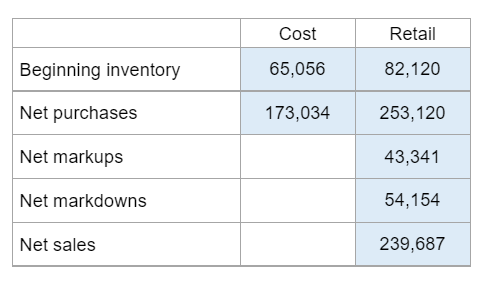

Find the conventional cost-to-retail percentage.

Your numbers will vary.

What is the process involved in using the dollar-value LIFO retail method for inventory?

What is the first step to take when using the dollar-value LIFO retail method for inventory?

What does the second step involve when using the dollar-value LIFO retail method for inventory?

How can one determine whether an increase in inventory value using the dollar-value LIFO retail method is due to an increase in quantities of goods rather than a change in prices?

How is the value of a LIFO layer determined under the dollar-value LIFO retail method?

What are the requirements when changing from the average cost method to FIFO?

If a company overstates its ending inventory in the current year, how does this impact the amount of reported cost of goods sold for the year?

What is the true statement regarding a company that overstates its ending inventory in Year 1 and reports inventory correctly in Year 2?