Quiz – Howard’s Supply Co.

Intermediate Accounting

Spiceland, Nelson, and Thomas

10th Edition

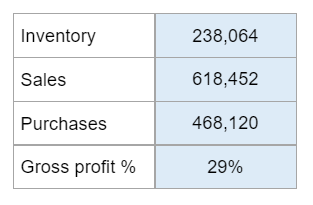

Find the estimated inventory loss.

Calculator Preview

Your numbers will vary.

Find the estimated inventory loss.

Your numbers will vary.

When costs are falling, inventory quantities stable, the lowest taxable income is reported by using which inventory method:

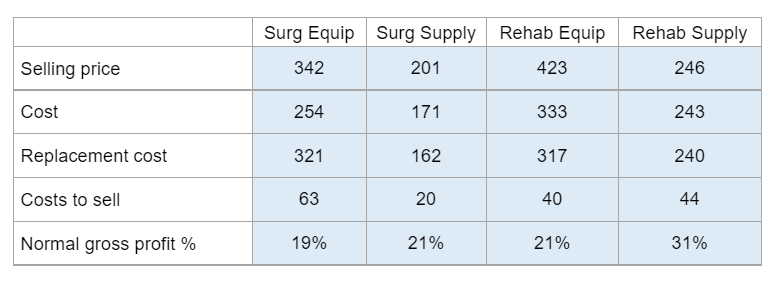

What will the inventory of surgical and rehab equipment and supplies be valued?

Your numbers will vary.

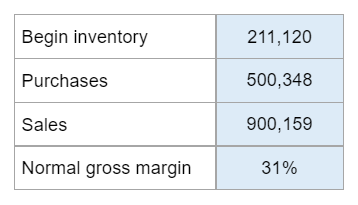

Compute the estimated cost of inventory lost in the fire.

Your numbers will vary.

In applying LCM, market value can’t be:

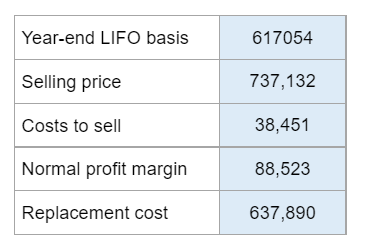

What should be the reported value of the company’s inventory?

Your numbers will vary.

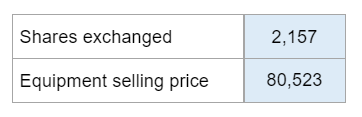

What does the journal entry to record the equipment transaction include?

Your numbers will vary.

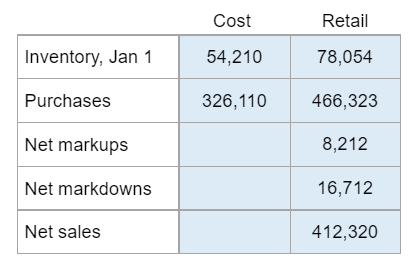

Estimate the ending inventory and cost of goods sold (Average Cost Method).

Your numbers will vary.

Find the average cost-to-retail percentage.

Your numbers will vary.

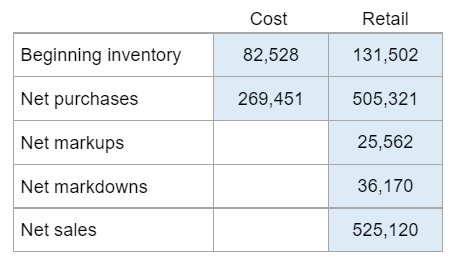

What is the estimated ending inventory and cost of goods sold under the Average Cost Retail Method?

Your numbers will vary.