Problem 20-20, Facebook

Principles of Corporate Finance

Brealey, Myers, and Allen

13th Edition

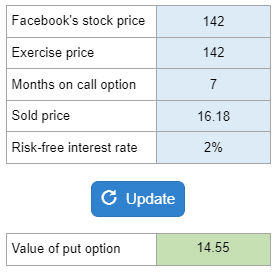

Given the stock price, exercise price, months on the call option, price it sold for, and risk-free rate… calculate the value of the put option.

Calculator Preview

Your numbers will vary.