E6-19A – Average Cost, FIFO, & LIFO

Financial Accounting

Thomas, Tietz, and Harrison

12th Edition

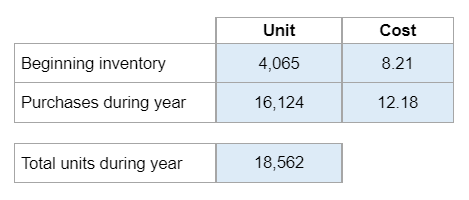

Using average-cost, FIFO, and LIFO – find the cost of goods sold and ending inventory.

Calculator Preview

Your numbers will vary.

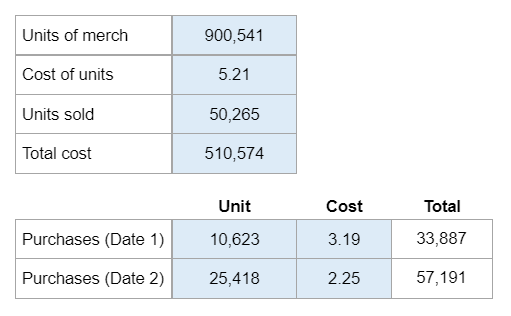

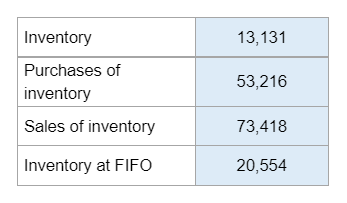

Using average-cost, FIFO, and LIFO – find the cost of goods sold and ending inventory.

Your numbers will vary.

Find gross profit under both FIFO and LIFO.

Your numbers will vary.

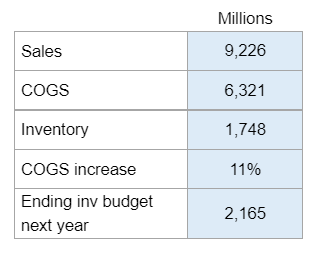

Determine how much inventory should be purchased during the upcoming year to reach budget.

Your numbers will vary.

Identify another reason that owners and managers use the gross profit method to estimate inventory.

Your numbers will vary.

Given the beginning and ending inventory, sales, and purchases – make the journal transactions under the perpetual system and find the ending inventory and gross profit.

Your numbers will vary.

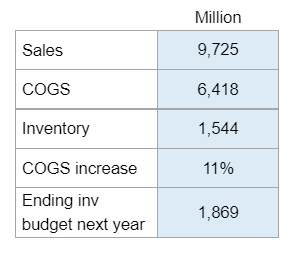

Determine how much inventory should be purchased during the upcoming year to reach budget.

Your numbers will vary.

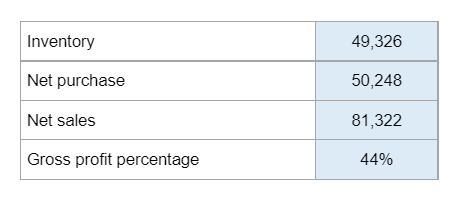

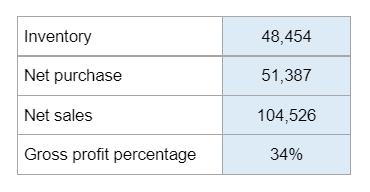

Given the information on inventory, net purchases and sales, and gross profit percent – estimate cost of inventory and find another reason managers use gross profit method to estimate inventory.

Your numbers will vary.

Given the inventory transactions for the corporation — prepare the journal entry using the perpetual inventory system and show what the corporation will report.

Your numbers will vary.

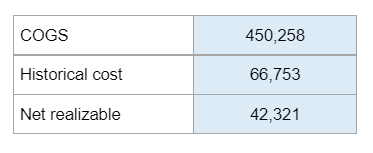

Given COGS, the historical cost, and net realizable — figure out what the company should report for ending inventory and COGS, along with which statement it would show up on.

Your numbers will vary.

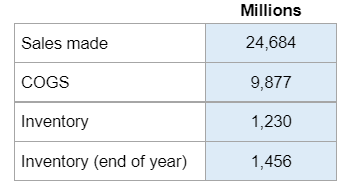

Given the sales made, COGS, and inventory at the end of the year — find the gross profit and the rate on inventory turnover.

Your numbers will vary.