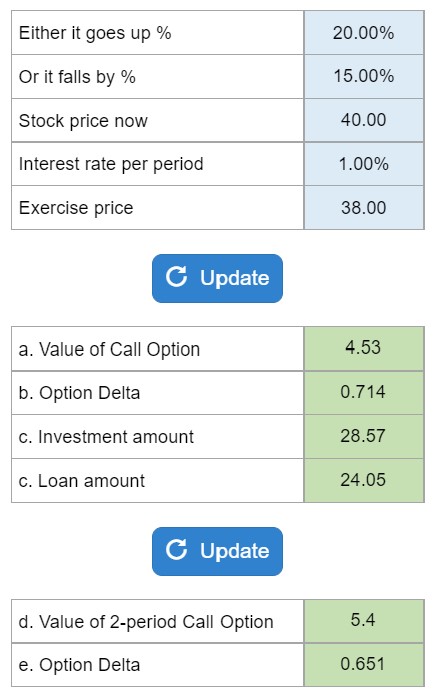

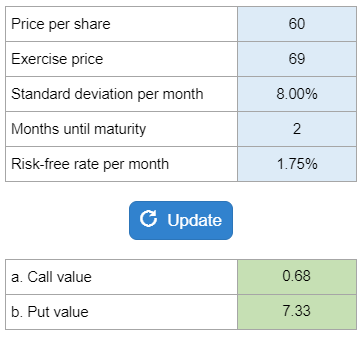

Problem 21-01, Ragwort Call Option

Principles of Corporate Finance

Brealey, Myers, and Allen

13th Edition

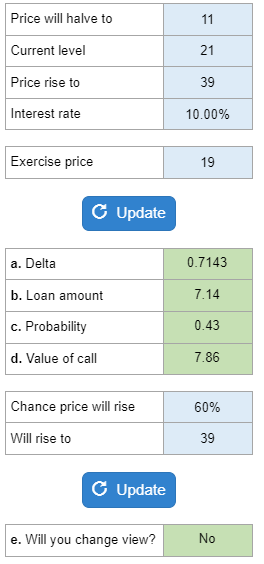

Determine the delta of a one-year call option, the risk-neutral probability that Ragwort stock will rise, and if you would change your view about the value of the option.

Calculator Preview

Your numbers will vary.