Quiz – DK Super Stores Inc.

Intermediate Accounting

Spiceland, Nelson, and Thomas

10th Edition

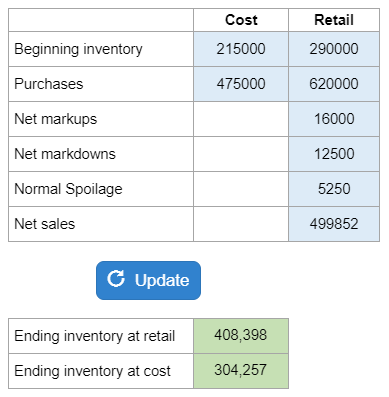

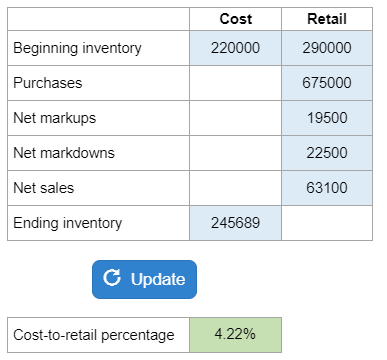

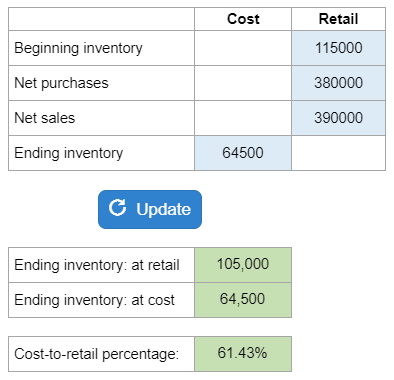

Given inventory, net purchases, net sales, and ending inventory, they ask you to calculate the cost-to-retail percentage used.

Calculator Preview

Your numbers will vary.