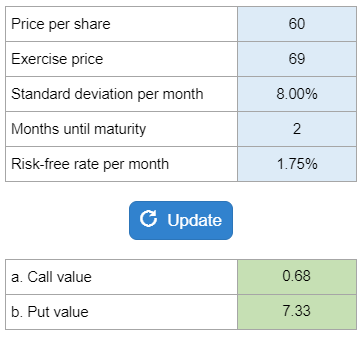

Problem 21-12, Black-Scholes Option Valuation

Principles of Corporate Finance

Brealey, Myers, and Allen

13th Edition

Determine the call value and the put value using the Black-Scholes formula given a monthly standard deviation and monthly risk-free rate.

Calculator Preview

Your numbers will vary.