Quiz – Portman Inc.

Intermediate Accounting

Spiceland, Nelson, and Thomas

10th Edition

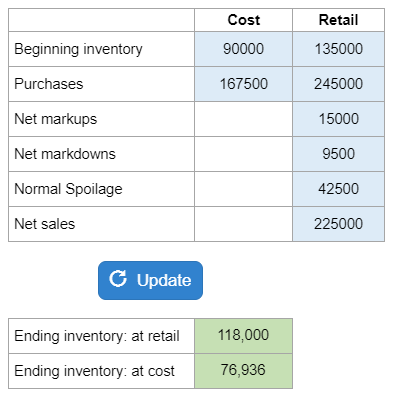

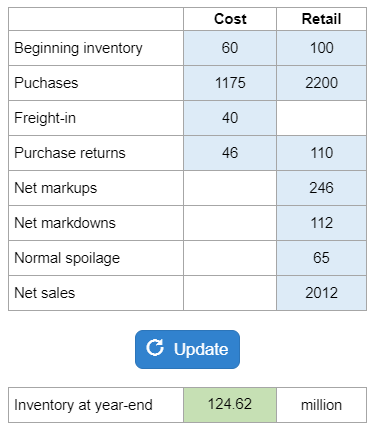

Given information about the inventory account, they ask you to determine the value of the inventory using the conventional retail inventory method.

Calculator Preview

Your numbers will vary.