Problem 3-05, Treasury offer

Principles of Corporate Finance

Brealey, Myers, and Allen

13th Edition

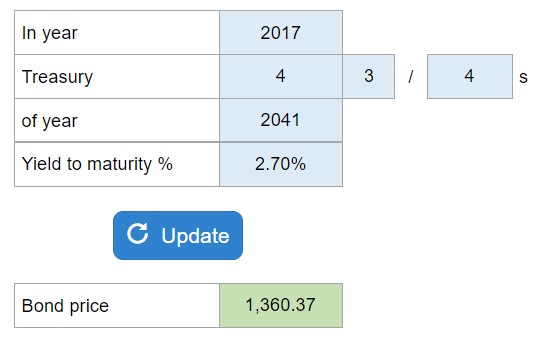

Determine the bond price assuming that coupons are paid semiannually on the treasury offering.

Calculator Preview

Your numbers will vary.

Determine the bond price assuming that coupons are paid semiannually on the treasury offering.

Your numbers will vary.

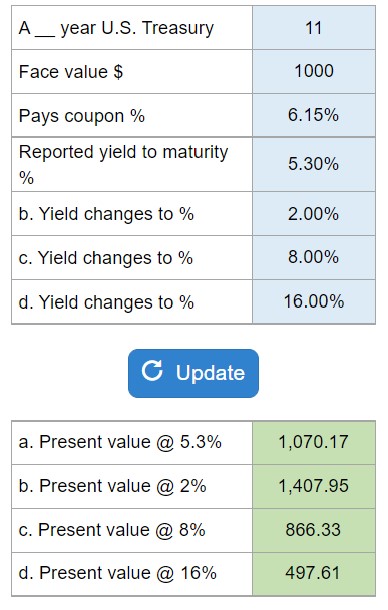

Determine the present value of the bond at various yields.

Your numbers will vary.

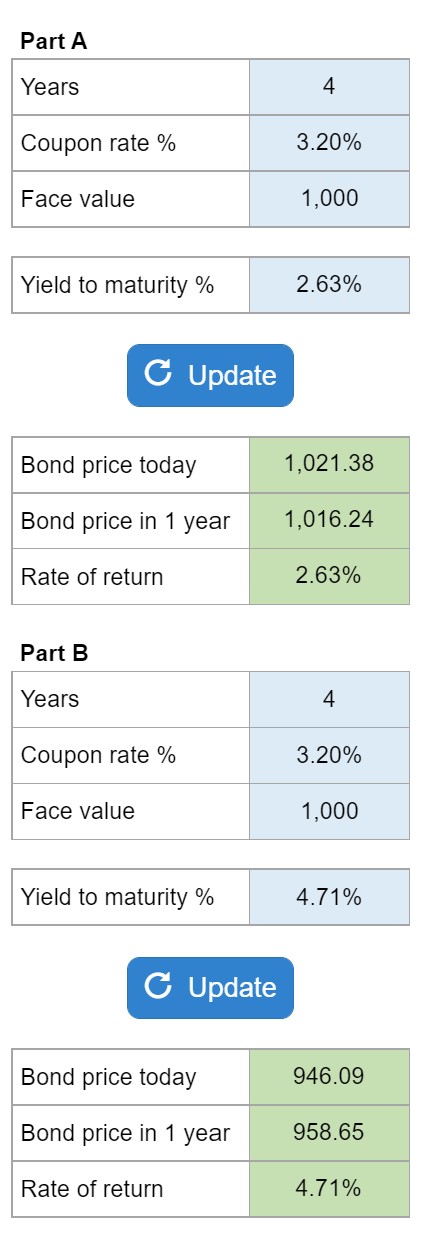

If a bond’s YTM doesn’t change, determine the bond price today, the bond price in one year, and the rate of return over a one-year holding period.

Your numbers will vary.

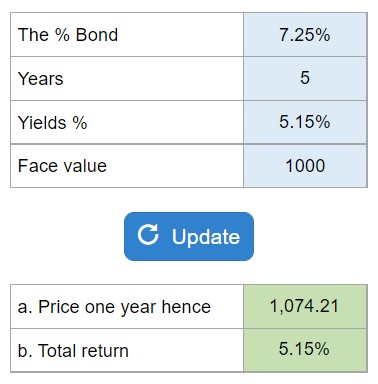

Determine the bond price after one year passes and estimate the investor’s total return who held the bond over the year.

Your numbers will vary.

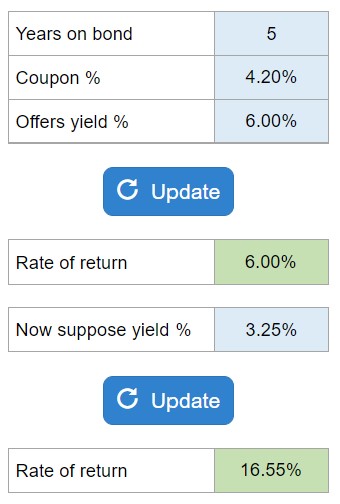

What rate of return does the bondholder earn over the 12-month period? If bond yields change, what rate return does the bondholder earn in that case?

Your numbers will vary.

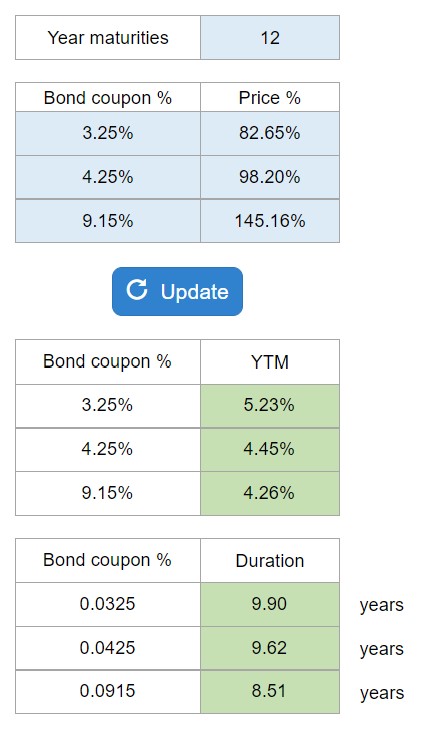

Calculate the duration of three different bonds after you estimate their yield to maturities. Which bond has the highest/lowest yield? Which bond had the highest duration and which one had the lowest duration?

Your numbers will vary.

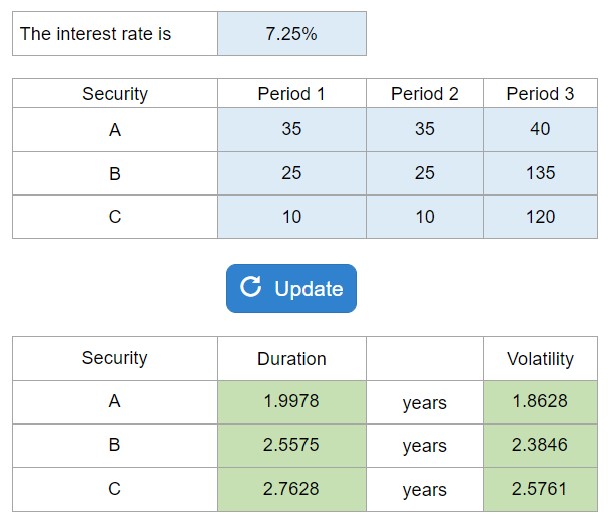

Compute the durations and volatilities of securities A, B, and C.

Your numbers will vary.

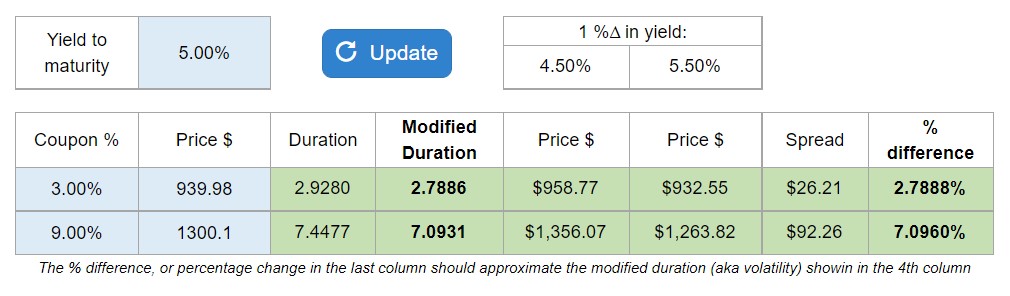

Compute the durations and modified durations for the bonds. Use the modified duration to estimate the percent change in the value of the bond given a 1% change in interest rates.

Your numbers will vary.

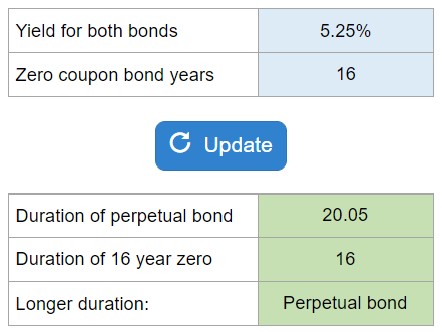

Determine the duration of a perpetual bond and zero-coupon bond. Which has a longer duration?

Your numbers will vary.

In the market for U.S. Treasury bonds, what comes first and what comes after? Spot rates, yields, bond prices? How are they related?