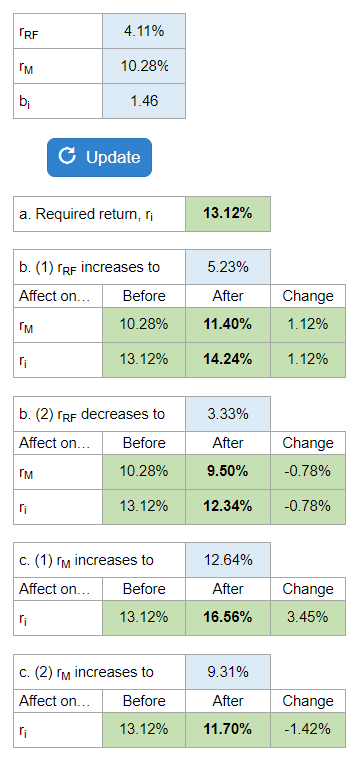

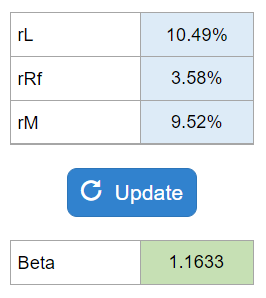

Problem 8.08 – Beta Coefficient for Stock L

Fundamentals of Financial Management, Concise

Brigham and Houston

09th Edition, 10th Edition, and 11th Edition

Determine the beta coefficient for Stock L that is consistent with equilibrium.

Calculator Preview

Your numbers will vary.