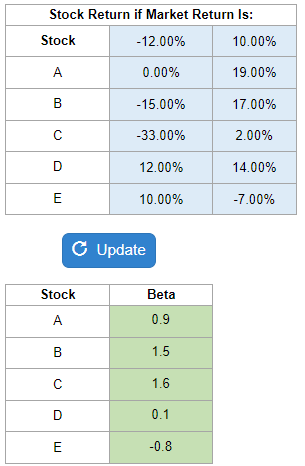

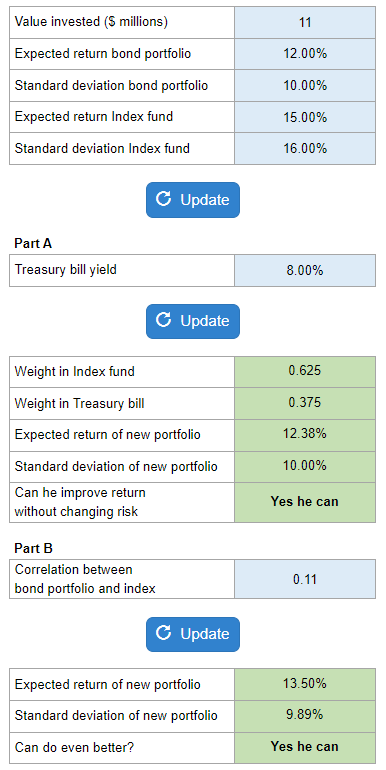

Problem 7-09, Diana Sauros Ace Mutual Fund

Principles of Corporate Finance

Brealey, Myers, and Allen

13th Edition

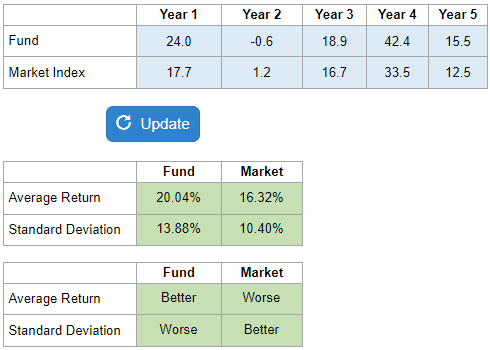

Given rates of return for a mutual fund manager and returns on the market… find the average and standard deviation of each.

Calculator Preview

Your numbers will vary.