BE 05.13 – Worthy Company’s

Financial Accounting

Spiceland, Thomas, and Herrman

05th Edition

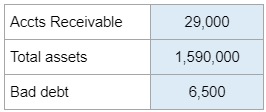

Given the accounts receivable, total assets, and bad debt… prepare a journal for the write-offs.

Calculator Preview

Your numbers will vary.

Given the accounts receivable, total assets, and bad debt… prepare a journal for the write-offs.

Your numbers will vary.

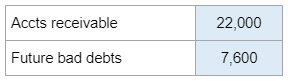

Given accounts receivable and future bad debts… record any necessary adjustments.

Your numbers will vary.

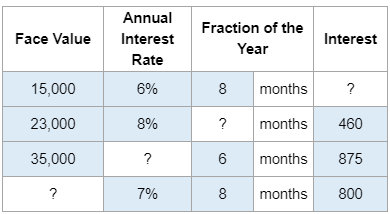

Given a table with face value, rates, the fraction of year, and interest for different notes… fill in the missing information.

Your numbers will vary.

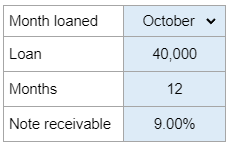

Given information on a loan that was lent out… calculate the interest revenue for two years.

Your numbers will vary.

Given information on a loan that was lent out… calculate the interest revenue for two years.

Your numbers will vary.

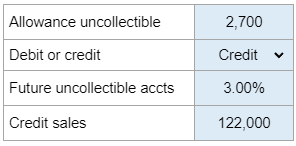

Given the allowance for uncollectible accounts, the estimated future uncollected accounts, and lastly the credit sales… record the bad debt expense.

Your numbers will vary.

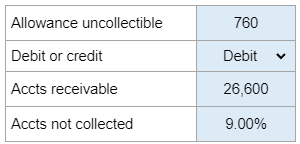

Given the balance in the allowance uncollectible account, the balance of accounts receivable, and the percent not collected… record the allowance of uncollectible accounts.

Your numbers will vary.

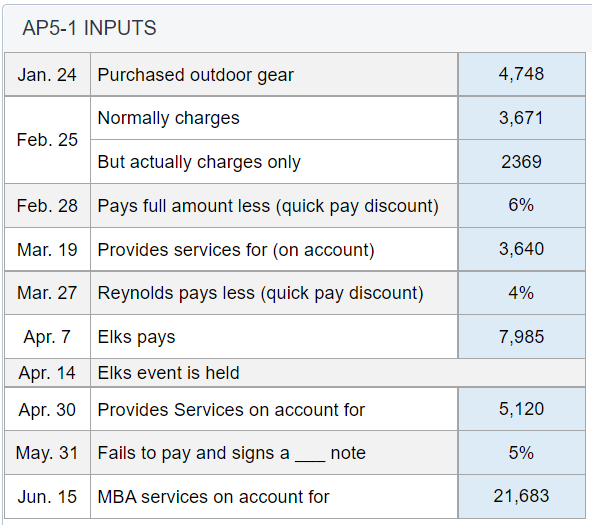

Prepare journal entries, partial balance sheets, evaluate the allowance of uncollectables, create a partial income statement with sales revenues, cost of goods sold, and gross profit. Calculate cost of goods sold and ending inventory using FIFO.

Then, using information about the net realizable value, reestimate the partial income statement and balance sheets. Finally, create a depreciation schedule showing depreciation and book values and record adjusting entries for depreciation and insurance.

Your numbers will vary.

Record the service on account and collection of cash.

Your numbers will vary.

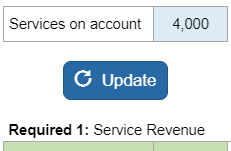

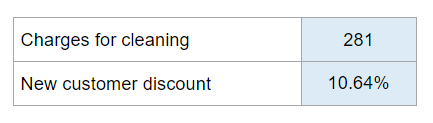

Offering a new customer discount. Record the revenue on May 1.

Your numbers will vary.