Problem 5.06 – Andreas Broszio (Geneva)

Calculator Preview

Your numbers will vary.

Difficulty – Medium

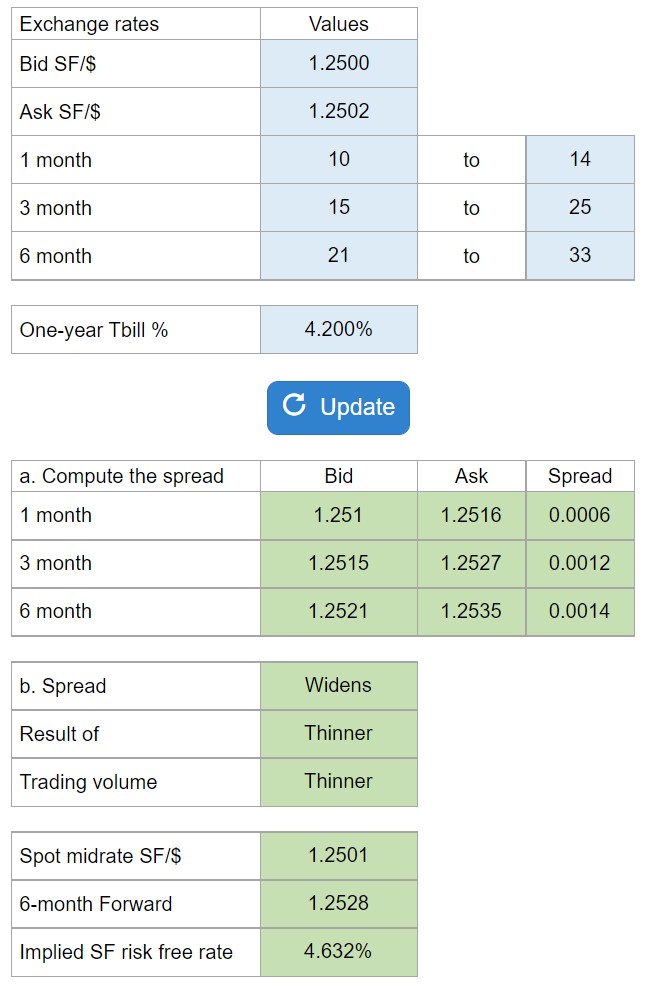

Given bid rates and ask rates along with a 1-month, 3-month, and 6-month forward, compute the Bid, the Ask, and the Spread. Finally, estimate the implied interest rate for the SF.

Experts Have Solved This Problem

Please login or register to access this content.